WorkWave Fintech

Increase sales orders, provide a better customer experience and reduce costs on a single platform.

Hi. I'm Heather Sugg, reporting for FinTech Futures from Money twenty twenty USA. I'm pleased to be joined today by Jacob Olins from WorkWave. Welcome. Nice to be here. Thanks for having me. Thank you. So, Jacob, you are VP of fintech at WorkWave. Tell us a little bit about your role and about yourself. Sure. So I've got a, history and started in banking. Started in financial services and, payments innovation group in, at Citibank. And then over the years, just had more and more of an affinity for, software platforms and the ability to distribute financial services through software platforms. So, WorkWave is a vertical SaaS platform that, supports field services companies. And I lead the financial services, what we call the fintech business unit there. We do a lot of payment processing. We do some lending. We do some payroll, earn wage access, a whole bunch of different, products that we've got that basically support our customer's businesses and are generally adjacent to money movement. K. Generally adjacent to money movement. I like it. Yes. There's a broad spectrum that you touch on. There's a lot of stuff. Yeah. There's a lot of opportunities. Who's a typical customer for you? A typical customer for us would be a a small or medium sized, in some cases, large enterprise business that runs a field services business. So that might be a a general contractor of some sort. It might be a, somebody who mows your lawn. It might be a a business that does janitorial work or security common theme is typically you're using trucks to, to mobilize a mobile workforce and perform services in the field. Cleaning, security, pest control is a big one. You're running that business. You're communicating with your employees where they need to be, what jobs they need to do when they're there. And you do all that on our platform and through our mobile application and back office applications. And then very pertinent to people that are out in the field, you have your own payments processor. So how does that apply to them and how is it being used? Yes. Absolutely right. So we're, we're a PayFac. We are our own payment processor. What it does is it allows us to tailor our payment services really to the needs of our specific customers. So a lot of our customers have a big portion of their business on subscription billing. Their customers are signing up for, a monthly lawn care service or a monthly pest control service. And so we're tailoring into our payments offering things like account updater. So that if they've got a card on file and that card expires or it's closed, or canceled, we're automatically tokenizing the card and so that service never gets interrupted. Our customer never has to reach back out to their customer, in order to to capture another card. So that saves them a lot of time. And then what we do is we try to look at, hey. What are all the different ways that our customers are, are taking revenue? And so, you know, a big portion of that is recurring services. That's usually a credit card payment. Another portion of that is gonna be commercial services, and so we'll facilitate ACH payments for, for those kinds of services. And then a a portion, typically, twenty to thirty percent of a lot of our businesses is large ticket services. So that might be a fumigation job in the pest control industry. There might be a tree trimming job in the landscaping industry. And that's a large service that many consumers don't have the money to to pay for that, but it's an emergency service, you know, on a big tree branch falling on, on your house. And so we offer financing as well. And so our customers are able to finance their customers. They get paid in full as soon as the, service is complete. And then we take over that collection from the from the consumer of the team. Yeah. And that's benefit on the consumer side as well than having that be a seamless or like, yeah, easy process for them. Yeah. Absolutely. Yeah. Easier process and funding when when they need it because a lot of these services are are essential. Vital. Exactly. So what does critical mass look like for you? For, for for us and for the fintech business unit, we've got a lot of opportunity and a lot of different, money adjacent sort of flows. And so, you know, the the payments acceptance product, that's our most scaled product. That's definitely at critical mass. Virtually, every one of our customers is uses that for the majority of the payments that, that that they're accepting from their customers. What we're really working on now is expanding more and more of those financial services offerings. So I think, you know, we we do it in the same way. We will oftentimes launch a partnership first, see if that's really resonating, and then we build into our product the experience so that it really seamlessly fits into our customers' workflows. So let's say, Financier, as an example, that's a newer product for us. You wanna offer that to the technician at the right point in their process. So if they're out doing an inspection, they're quoting a service, you want them to know, hey. I can offer this financing and not just, hey. It's available, but this I can give you this job for five thousand dollars or x installing payments of a hundred and fifty dollars a month. We want them to have it in context so that they don't have to think about, oh, can we offer financing on this job? Can we not on that job? Right? They're they're there to do a job. They're there to perform a service. And then we want our mobile application and our platform to to make any of that money movement, financial related activity super, super obvious and and not require, like, additional training. Do you find that the financing options are increasing spending power? Yeah. That's a that's a that's a really good question. I I think, when a technician is is able to have some of the insight into what a customer can afford to spend, they might recommend different services than than they would otherwise. So, you know, if you're totally blind to your customer's financial situation, you might air one way or another way that might actually alienate the customer from that sale. If you're getting more insight, it's obvious that the customers is the one opting in in the first place. They're saying, you know what? I'm interested in financing. Then then we're able to provide our customers with visibility into what that financing might be. And they might say, you know what? You gotta turn my job. It's absolutely essential. We gotta get we gotta do that. But we've also noticed there's some, holes where some rodents are crawling in, and maybe it's a less significant service, but customer's happy to have everything done that they need done at that point in the can. That's fantastic. What's coming next down the pipeline for you in financial services? A couple of big things for us this year. We we've got a a bill pay product that's gonna be coming out, early next year. That's really exciting for us. It's gonna enable our customers to basically outsource their entire accounts payable process to us. It's gonna save a lot of time for our customers. It's gonna, reduce a lot of error rates. And and the customers that are most excited about this, what what they're saying to us is, hey, I'm I'm spending time every week supporting three or four different accounts payable processes. If you can sort of turn that into one and reduce the error, then I can take that that staffing power and put them on higher value projects for me rather than than just, you know, auto being in the narrow tracking. Yeah. That was really that was a really cool conversation I had just last week. We've got a this customer is who's excited about our build a product. They're also moving on to our payroll product. And that's another area where we've got some really exciting innovations. Earn wage access has has been a really, really powerful, employee retention tool. And so we're we're deepening our earn wage access product to make it just much more accessible for our, customers' employees. How are you deepening it? Just embedding that, user experience right into the product. So, you know, historically, Earned Wage Access is something that, employer will sort of socialize to their employees, And depending on how engaged their HR department is or what kinda communication strategy they've got with their employees, their employees might not be aware of all the benefits that they're providing to their employees, as an employer. And so we're able to use that same real estate that these employees are using every day to punch in, punch out, know where they're going, what they're doing, to help our employers effectively market to their employees. Hey. Here's some additional services that you're getting, you know, as as, a virtue of being an employee of this company. Very nice. Now WorkWave is somewhat unique in the fact that, a lot of what we're seeing here in the vendors at twenty twenty are, with VC companies, and they are stabilizing their growth through that. We heard from, in the New York Stock Exchange about what they're expecting with IBOs. But you've gone the PE route. Tell me about what you why you decided to do that and how it's affecting your business. Yeah. I I think, Workway has been really successfully private equity owned for a number of years. I think, you know, it comes with, with a different set of, opportunities and and constraints. I think one of the things that that, you know, encourages us to do is just be really resourceful. And so, you know, we're we're gonna be more inclined to to launch a partnership as a way to validate whether, a product is gonna be a fit for our customers than try to build something, you know, big up up front. So I think just operating, you know, within constraints makes us, more thoughtful about the products that that we're bringing to market, makes us more thoughtful about the customer experiences that we're bringing to market. And I think, you know, it goes a long way and and we've got the customer loyalty to, to to prove it. Yeah. And so given your years of experience in private equity, how what would you advise for companies about how to remain competitive in that space? Yeah. I think, you know, I think the, the financial services and it's such a niche. Right? But it's like vertical software. You're used to selling software. You always think about software. And so a lot of the financial services opportunities are just not second nature to your your customers or take advantage of these, services one way or another today. They're probably procuring something from a bank. The value that you've got and the experience that you provide as the vertical software provider, the data that probably your customer is already using, but in a really clunky way in order to to procure the financial services that they need, you can do that for them. I think that's that's one of the biggest pieces of advice is that I would give it. Look at where does your product support money movement? Are you in the accounts payable flow? Are you in the accounts receivable flow? Are you in anywhere that money has moved, the the payroll flow? Do you have any kind of insight into how that money is being spent or being earned? You probably have a really big financial services opportunity that you might not be capitalizing on. Very nice. I like it. Well, Jacob, is there anything else you'd like to add? I I think that's, about it. Yeah. This seems really wonderful. Thanks so much for having me. It's been lovely. Thank you.

Top Fintech Features

Achieve Greater Ticket Sales With WorkWave Payments

- 83% of small businesses that accepted credit cards saw an increase in sales

- 85% of customers prefer to pay with credit cards for field services

- Elimination of manual, double entry operations due to streamlined, integrated payment processing

- 90% of Americans are making payments using a credit or debit card

Multiple Payment Options to Increase Customer Satisfaction

- Delight customers with multiple ways to pay from a service provider they trust

- Credit cards, debit cards, ACH, ePay invoice links and more

- Improve customer satisfaction and loyalty by encouraging credit card payments

- 5% higher customer retention rates increase profits by 25% or more

Trust and Transparency

- Reliable cash flow with daily payouts

- Daily summaries and easy to understand reporting

- One support center for all of your needs

- Highest level of PCI compliance and payment data protection

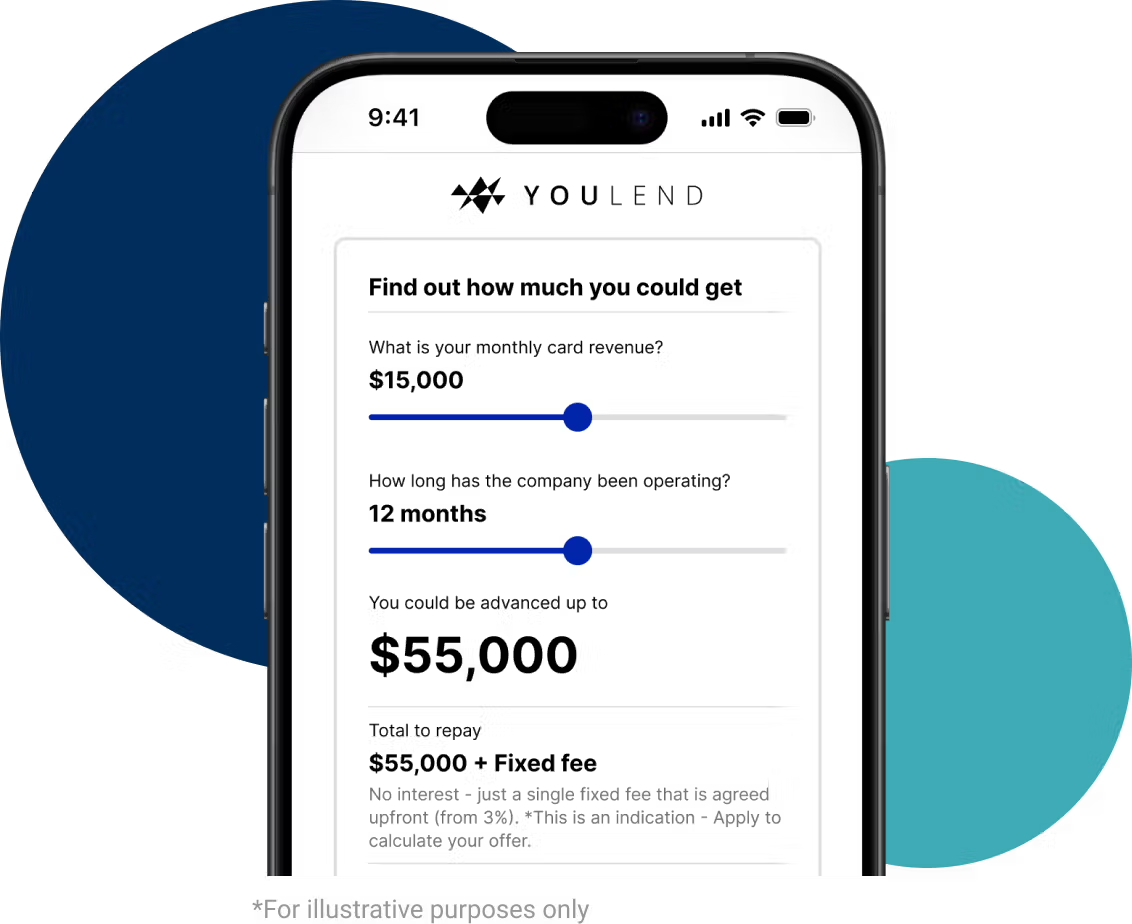

WorkWave Capital

- Borrow anywhere from $1,000 to $1 million

- Access funds in as little as 24 hours

- Cash for whatever you need, when you need it

- Easily cover unexpected expenses

- Take advantage of time sensitive opportunities

*Funding is provided by YouLend; WorkWave is not providing the credit. Prequalified offers are based on sales and are subject to a credit check. YouLend terms and conditions apply.

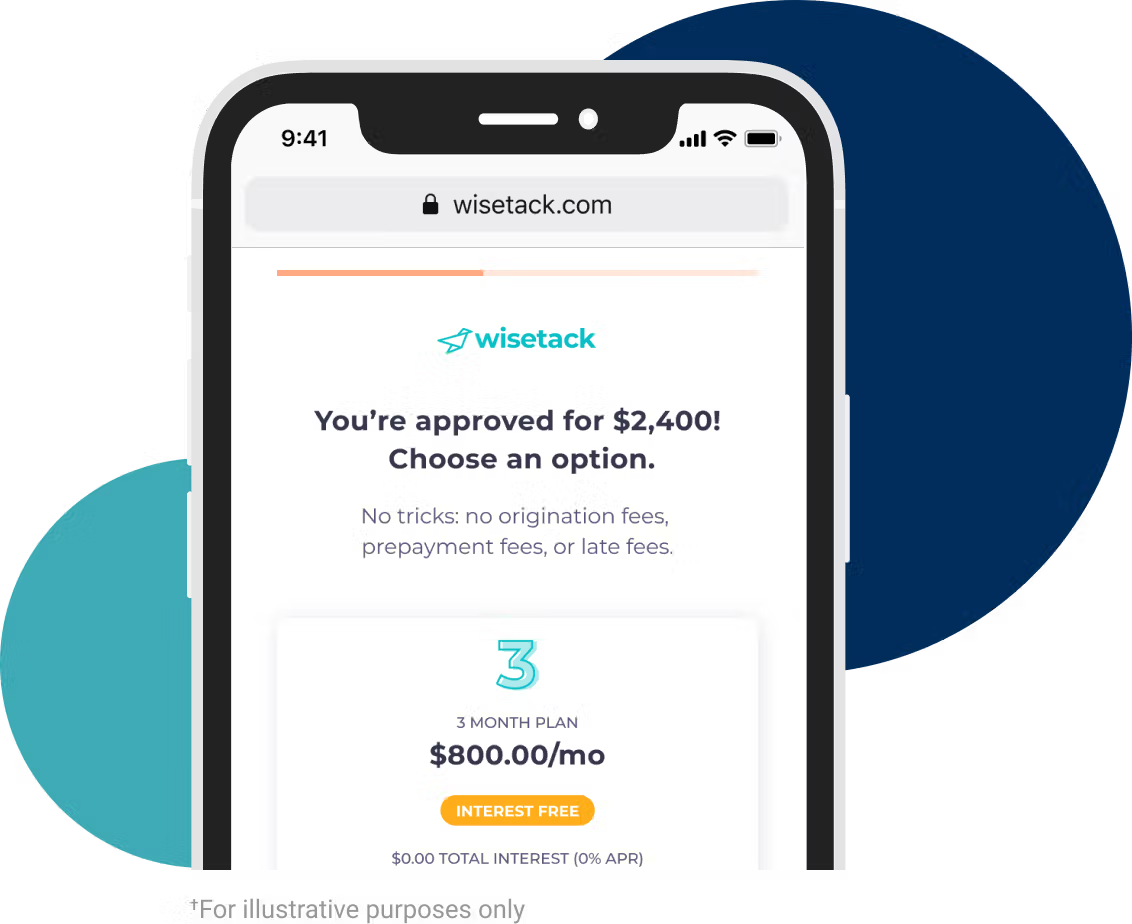

WorkWave Pay Over Time

- Give your sales team a new tool to close more and bigger jobs

- Offer pay-over-time options with a click of a button or via text

- Customers can finance jobs between $500 - $25,000†

- You can get setup in under 5 minutes with no start up or annual fees

†All financing is subject to credit approval. Your terms may vary. Payment options through Wisetack are provided by our lending partners. For example, a $1,200 purchase could cost $104.89 a month for 12 months, based on an 8.9% APR, or $400 a month for 3 months, based on a 0% APR. Offers range from 0-35.9% APR based on creditworthiness. State interest rate caps may apply. No other financing charges or participation fees. See additional terms at https://wisetack.com/faqs.

Trusted by 375,000+ service professionals

It's very irritating to customers when they can't pay their bill. By moving over to Workwave payments, the guys can enter the payments in their phone They just enter the card number on the app, and it processes the payment, records the payment in Workwave, and it's all done in one transaction. So Workway payments has really helped because our customers can go in and access the customer portal and make their payments directly through that portal. So our CSRs aren't taking phone calls, spending five minutes talking to miss Smith while she digs through her purse looking for her credit card. Definitely improved that level of efficiency. With Workwave payments, we send them the invoice and they have a pay now button and the customers use that all the time. They love being able to just click the button, enter their credit card, and then pay that one invoice.

Our Customers

Still Have Questions?

Looking to Grow? We've Got You Covered.

Interested in learning how to grow your business and better serve your customers? Check out our resources!